Receiving a Bonus or Retirement Allowance? Don't Let the “Tax Filter” Eat Your Lump Sum

Whether you are transitioning to a new career or approaching your final shift, receiving a retirement allowance (or severance pay) is a significant financial milestone. While it feels like a windfall, it comes with a complex set of decisions that can impact your long-term wealth.

It's not just about the numbers

Many clients come to me asking for a mathematical comparison of their options. While the math is important, it shouldn't be the primary driver of your decision. Before crunching numbers, you must evaluate two things:

Control and ownership — If you leave your funds within an employer's system or a union-controlled plan, you lose flexibility. Taking the lump sum allows you to bring that money “into your fold,” giving you full supervision over how it is invested, as well as when and how you use it.

The “worst-case” scenario — What happens to that money if you pass away prematurely or become disabled? By taking the allowance and moving it into a personal account like a LIRA or RRSP, you can name your beneficiaries and ensure the assets are protected for your family.

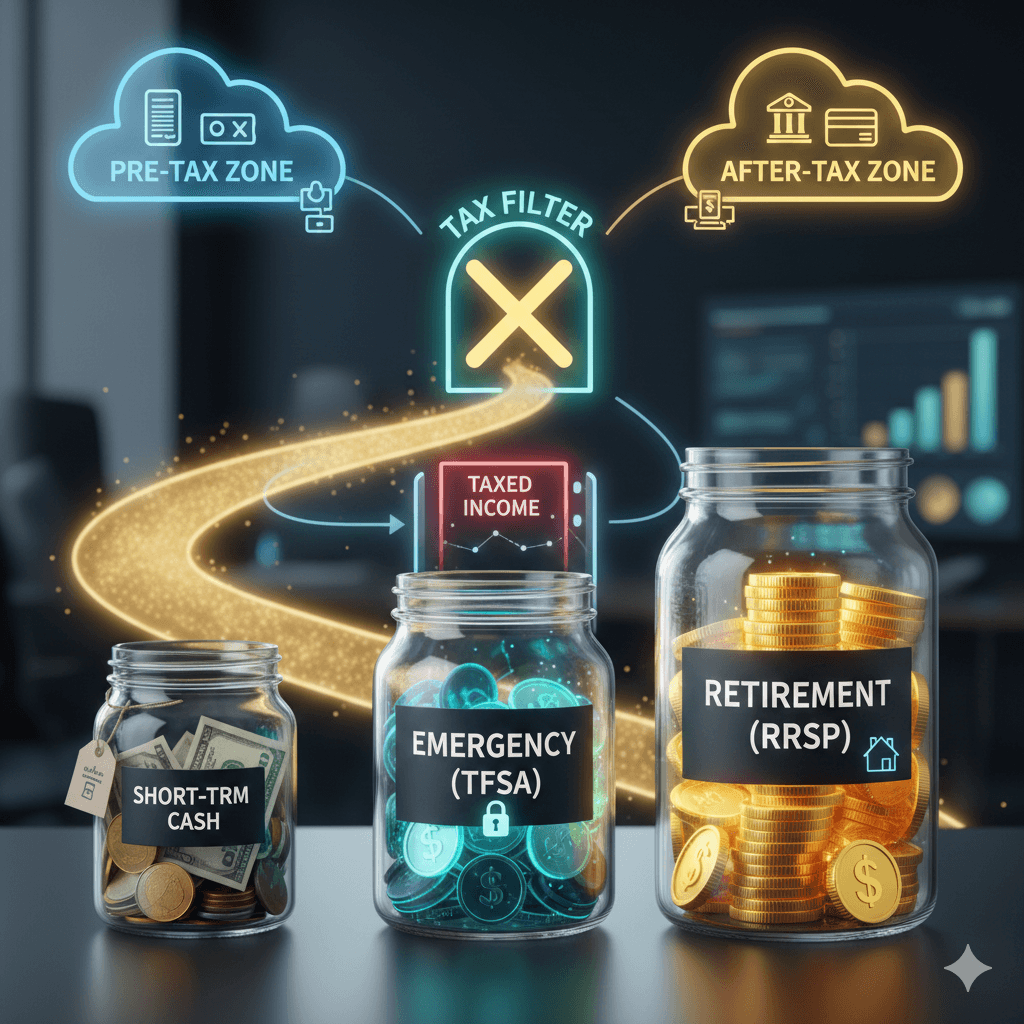

Navigating the “tax filter”

To visualize your options, think of the Pre-Tax vs. After-Tax money illustration. Your pre-tax zone includes your income, pensions, and RRSPs; your after-tax zone is your bank account and TFSA.

When you receive a retirement allowance, it is taxable as income. If you take the cash upfront, you might lose up to 40% or more to the CRA immediately. However, if you have sufficient RRSP contribution room, you can often transfer the allowance directly into your RRSP without the “tax filter” taking a bite. This keeps the full amount working for you, with taxes deferred until you actually need it in retirement.

The cascade of accumulation

Planning for a lump sum requires looking at your “buckets” of savings:

- 1.Short-term / cash: for immediate needs such as travel or renovations.

- 2.Emergency (TFSA): your flexible bucket. Since withdrawals are non-taxable, it's the best place for unexpected costs in retirement.

- 3.Retirement (RRSP): this bucket replaces your monthly income, it pays the groceries and keeps the lights on.

When deciding where to put your allowance, we look at which bucket is empty. For some, it makes sense to pay a little tax now to fill the TFSA for future flexibility. For others, maximizing the RRSP to defer taxes is the winning strategy.

If you're preparing for retirement and want to explore how best to structure your accumulation buckets and income streams, I'd be happy to help. Reach out today, and let's start crafting your personalized wealth plan.

Want this applied to your numbers?

Book a free intro call with Marcel — no pressure, no sales pitch.